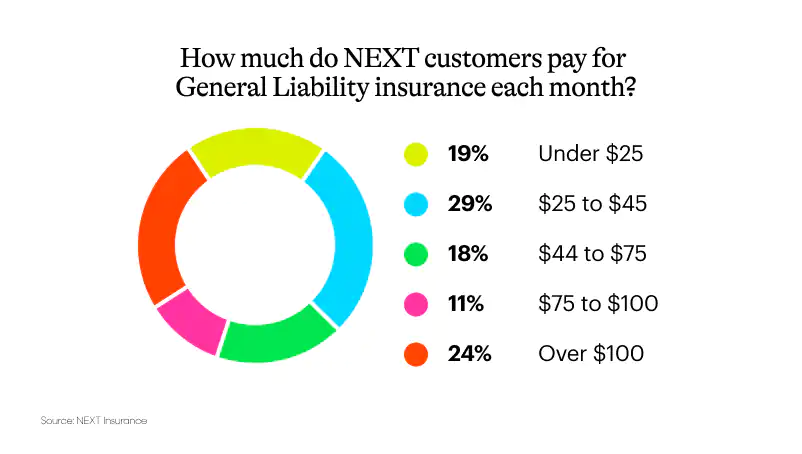

What factors influence the cost of general business liability insurance?

Your specific commercial general liability insurance cost is determined by several factors that are used to determine if your business has high-risk or low-risk business operations. These include:

The type of work you do

Higher-risk businesses could be more likely to have a claim involving an injury and property damage. In general, jobs that include working on other people’s property often have higher insurance costs.

Number of employees

If you employ seven people, your insurance could cost more than if you work alone.

Your claims history

Your record of losses and claims has an impact on your small business insurance costs.

Your work experience

For example, if you have 25 years of experience and no claims, you can probably expect to pay less than someone who’s been in business for two years and has experienced an insurance claim.

How high you set your limits

Higher coverage limits offer more financial protection, but will almost always increase the amount of your insurance premium. Still, you could pay less out-of-pocket if there is a claim.

The state where you work

This is partly due to different states having different regulations and partly because insurance rates are sometimes higher in densely populated areas that experience more business property claims.

These are only a few common factors that affect your costs. Insurance providers take into account many other factors, including external factors such as economic conditions and market trends.

Note: It’s important to provide the most accurate information about your business when you get a general liability insurance quote to ensure you get the right type of coverage and there are no delays in processing claims.

How policy limits impact the cost of General Liability insurance

General liability policies have per-claim limits and aggregate limits. Once the limit is reached, you’re responsible for paying whatever’s left over.

For example, say you have a general liability policy with a $500,000 limit with no deductible. If you damage a client’s home that will cost $600,000 in a single claim, you would have to pay $100,000 out of pocket.

If you want more protection from damages and incidents, you’ll need higher coverage limits, which would increase your premiums.

Many general business liability customers opt for a policy with at least $1 million limits. The appropriate coverage depends on individual needs and your financial risk tolerance.

How to reduce General Liability insurance costs

You can take several steps to reduce your general liability business insurance cost:

1.Bundle more than one policy

In addition to the risks general liability insurance covers, many businesses need more than one type of business insurance coverage.

You can save up to 10% if you purchase more than one type of business insurance with NEXT.

General liability insurance is often combined with commercial property for what’s known as a business owner’s policy (BOP) for additional savings.

Insurance packages also often include a combination of general liability and:

For example, if you add workers’ compensation coverage with your general liability policy, you could save 10% right off the bat.

2. Keep your risk level low

A safety and training plan can help limit the likelihood of filing insurance claims and raising your policy costs. For example, you might:

- Make sure you and your employees are properly trained

- Focus on work that you know how to do

- Don’t do jobs that you aren’t trained to do or didn’t get insurance to cover

- Make sure you have coverage for the work you do

- Keep your business or job site secure

- Keep your business and work area clean so no one trips on cords, furniture, equipment or tools

- Take steps to mitigate property damage and injuries from rain, wind, snow and inclement weather.

3. Learn from previous claims

Examine your previous claims history and determine what you may have done to avoid or lessen such risks.

4. Pick the right limits and deductible

Although lower limits will save you money, if you don’t purchase enough coverage, you could be more vulnerable to financial losses. Having higher deductibles may help you save some money.

Additional General Liability insurance resources

Frequently Asked Questions

Compare General Liability insurance

Related terms